What is the Job Demand, Career Prospects & Salary in Malaysia for Financial Technology (Fintech)

Financial Technology or Fintech is an all-encompassing term used to refer to technology in the financial services sector. Fintech used to refer to the back-end technology used to run traditional financial services organizations, but has morphed into a term primarily used to describe disruptive financial technologies.

Recent regulatory changes are driving FinTechs in Malaysia, with FinTech adoption rapidly growing in the country. Financial services are steadily expanding out of traditional banking spaces, and digital finance is on the rise, particularly across segments such as payments, e-remittances, wealthtech, alternative financing (such as Buy Now Pay Later) and cryptocurrency trading. These elements build on a maturing e-wallet industry that counts over 40 non-bank providers. Bank Negara has also released a licensing framework for digital banks, awarding licenses to five consortiums.

The country is also set to be the global leader in Islamic FinTech. Malaysia’s market maturity and high transaction volume in the field have helped it ranked first in the Global Islamic FinTech (GIFT) index.

While Malaysia is inevitably impacted by the most recent global tech slowdown, the country’s market position, multi-year plans, macro frameworks and recent developments will help the country’s FinTech industry recover and accelerate ahead.

Fintech now became a central part of Malaysia’s financial sector, with considerable scope for expansion, according to a recent IMF analysis. With its growing middle class, high mobile phone usage, and strong government support for the digitization of the economy, Malaysian businesses and consumers appear ready to embrace fintech technology. Digital payments and wallets are leading the way in Malaysian fintech, followed shortly by insurtech, digital remittances, blockchain, crowdfunding and other forms of financial technology.

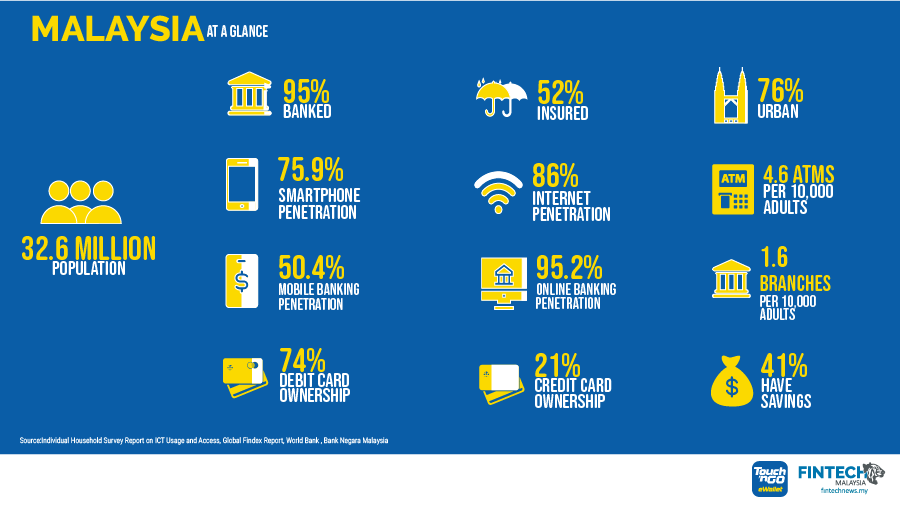

Internet banking in Malaysia quadrupled over the last decade, supported by 4G coverage and affordable data to promote mobile banking. The financial sector landscape also changed in the past few years, with physical commercial bank branches reducing and ATMs declining. All these statistics hint towards the fact that financial institutions started shifting towards adopting fintech, which is in sharp contrast to the initial scepticism it received from them.

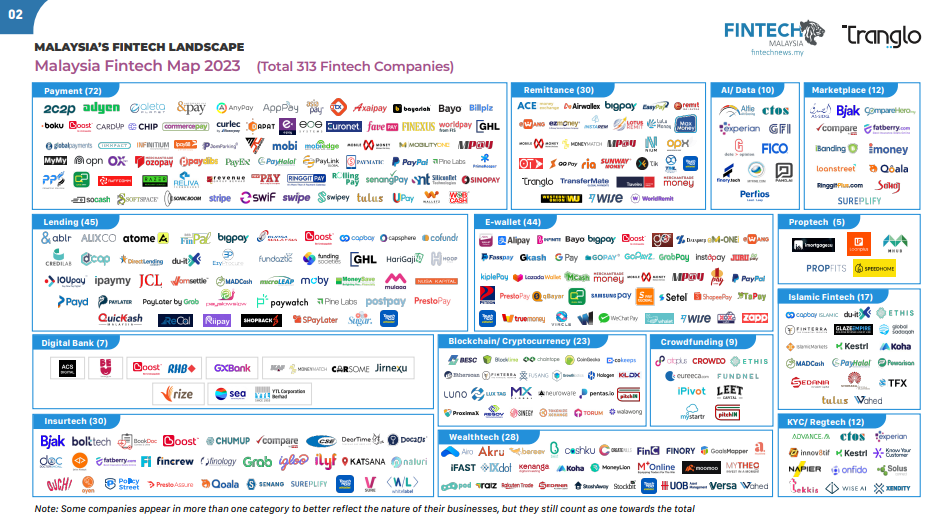

The Malaysia Fintech Market is highly competitive and fragmented as Malaysia is the largest market of the Fintech Industry throughout Asia. The Malaysia FinTech ecosystem is developing faster each year, with more companies and incumbents seeking new opportunities to collaborate, connect and co-create. It will cater to numerous clients and cover various services such as digital payments, alternative finance, wealth management, and blockchain. Malaysia groups such as MyCash Online, Jirnexu, and Mobi are focusing on innovating the FinTech industry and leading the Malaysia Fintech Market to new heights. Some major players are Jirnexu, MyCash Online, Capital Bay, PitchIN, MHub, etc.

Talent is a key challenge for companies looking to succeed in Malaysia’s FinTech sector. The rapid pace of digital transformation and rise of FinTechs have resulted in an insufficient local talent pool to meet every company’s demand.

You might also be interested to read:

- Top 5 Private Universities in Malaysia for Financial Technology (Fintech)

- Financial Technology (Fintech) is a Top Emerging Job in Malaysia with High Job Demand & Salary

- Best Financial Technology (Fintech) Degree Courses in Malaysia – What are the Subjects, Course Details & Entry Requirements,

- Best Degree Courses to Study for a Career in Fintech

- Financial Technology (Fintech) is a Top Emerging Job in Malaysia with High Job Demand & Salary

- A Fantastic Career Opportunity with Financial Technology (Fintech) as it has High Job Demand & Salary in Malaysia

- A Fantastic Career Opportunity with Financial Technology (Fintech) as it has High Job Demand & Salary in Malaysia

Financial Technology (Fintech) – The Job Demand, Career Prospects & Salary in Malaysia

The fintech umbrella includes insurance technology (insurtech), regulatory technology (regtech), financial data APIs, payments, banking, and mobile banking, among other types of technology. Each category represents a distinct category of finance-specific technology.

The explosion of the internet and the mobile internet has catalyzed the rapid development of financial technology. Even lumbering, highly regulated and highly cautious industries (such as insurance) have begun to embrace the innovative opportunities for enhanced effectiveness offered by fintech solutions.

Financial services institutions have warily kept fintech companies at arm’s length, seeing them as industry disruptors and potential competitors. Wisdom and self interest have triumphed over caution, it seems, as financial giants have started to invest in and partner with fintech companies.

This newfound acceptance and promotion of fintech innovation, proven by the large amount of investment in the fintech industry, will accelerate the development and implementation of fintech throughout the financial services sector.

Data from Bank Negara Malaysia shows that mobile banking transaction value has grown seven times in the past five years whereas e-money’s transaction value has grown more than double in the same period. This indicates that Malaysian are increasingly becoming more comfortable with using mobile financial services.

Fintech aims to make institutions more efficient and effective, provide consumers and businesses with more choices, increase transparency and cut down on the amount of time wasted during financial transactions.

Fintech Growth in Malaysia

Bryan & Wen Kai, Fintech at Asia Pacific University (APU)

In 2024, Malaysia is set to see significant growth in its fintech industry. This is primarily due to increased digital adoption in the country, supported by government regulations, substantial funding, and a growing talent pool. These factors are vital contributors to the increase in demand for qualified Fintech professionals in Malaysia.

The Malaysia Fintech Market size in terms of transaction value is expected to grow from USD 46.63 billion in 2024 to USD 96.09 billion by 2029, at a CAGR of 15.56% during the forecast period (2024-2029). The fintech landscape in Malaysia is evolving dynamically, marked by the innovation of local startups and global players introducing new business models, products, and services. Various segments within fintech, such as digital banking, Islamic fintech, insurtech, wealthtech, and payments, are experiencing rapid development.

Malaysia’s FinTech industry is one of the most developed in Southeast Asia. The government has also offered funding to upcoming innovators in the country’s fintech industry. There are a few entities that specifically finance the FinTech industry:

- Malaysia Debt Ventures Berhad

- Cradle Fund Sdn Bhd

- Malaysian Digital Economy Corporation Sdn Bhd

Furthermore, in 2022, Bank Negara Malaysia (BNM) has unveiled the 5 consortiums that will be getting a digital banking licence in Malaysia, as approved by the Ministry of Finance (MoF).

The advent of digital banking in Malaysia stands to not just disrupt the country’s financial and banking industries, but also jumpstart other fintech and digital payment companies in the same ecosystem. Malaysia will become just the second country in ASEAN to issue digital banking licenses, after Singapore, which issued four in 2020.

In addition to digital banks, the sector’s emergence stands to uplift associated services, such as e-wallets, digital investment platforms, and budgeting services, as well as other businesses seeking to integrate digital payment options into their platforms.

In line with the 5 strategic thrusts stated in the Financial Sector Blueprint 2022-2026, BNM will continue to work with the financial and fintech industries and relevant stakeholders to continuously enhance access to financial services throughout the country and across all segments of society.

Over the years, fintech has grown and changed in response to developments within the wider technology sector.

- Digital banking : Digital banking is easier to access than ever before. Many consumers already manage their money, request and pay loans, and purchase insurance through digital-first banks. This simplicity and convenience will likely drive additional growth in this sector, with the global digital banking platform market expected to grow at a compound annual growth rate (CAGR) of 11.5 percent by 2026.

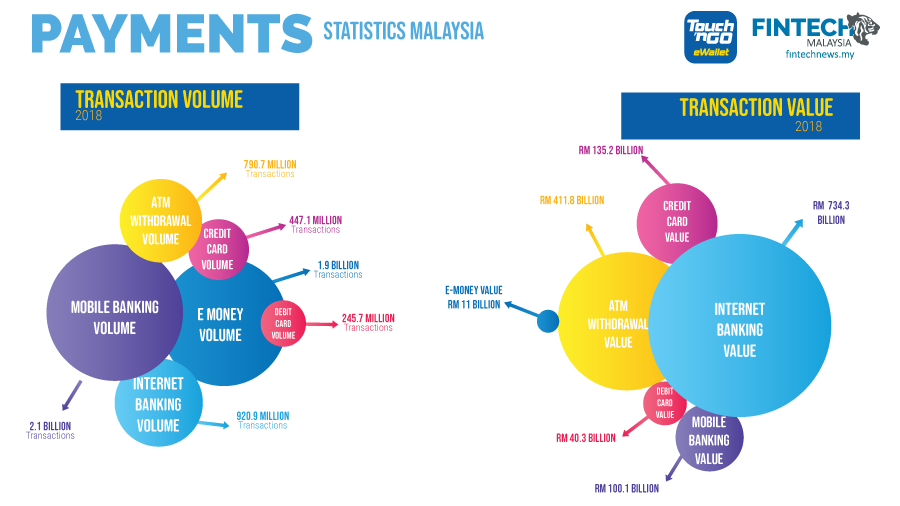

- According to The Edge Markets, the transaction value per capita increased from RM550,703 in 2016 to RM668,785 in 2018. The volume of e-payment transactions per capita rose, from 97.5 in 2016 to 124.6 last year. At the same time, reliance on cheques had reduced; the transaction value and volume per capita for cheques fell from RM52,646 in 2016 to RM44,215 in 2018 while volume reduced from 4.2 to 3.1.

- The Fintech industry of Malaysia has also grown with regard to the demand of Fintech companies in the country. A stunning 125% increase in mobile banking transactions were reported in 2020, with over 100% increase in E-remittance in 2020. This growth has allowed the fintech market of Malaysia to be able to challenge the markets of other countries and present itself as a major player in the regional fintech scene.

- Developments and changes to the Digital Laws of Malaysia also serve as proof of the growth of fintech in Malaysia. In December 2020, the central bank released a licensing framework for digital banks.

- The central bank, Bank Negara Malaysia, is working to raise the profile of FinTech amongst financial firms and insurers to improve the quality and efficiency of the country’s financial services sector. This push has created more job opportunities for candidates in the emerging technologies space including mobile and the web.

What are the Areas in Fintech and the Job Demand Globally?

- Insurtech

- Insurance technology (insurtech) saw over $2 billion worth of investment in 2017, a solid endorsement of the value provided by solutions in this fintech subcategory. Insurtech has been slowly embraced by the insurance industry, a notoriously un-innovative industry.

- The strict regulations that govern the insurance industry have held back the development and implementation of insurance-specific applications. Now, however, insurance agencies have embraced the potential represented by insurance-specific solutions.

- The global insurance industry gross written premium (GWP), which is essentially the size of the industry, was $4.8 trillion in 2017. There is massive potential in the industry, and the influx of insurtech investment will continue as fintech companies look to capture some of that huge market.

- Regtech

- Regulatory technology (regtech) is technology that helps financial institutions meet financial compliance regulations. Regtech has seen an immense upsurge in popularity within the past few years, which is due in part to the rise of disruptive fintech products.

- Regulators have scrambled to shackle these new technologies to protective regulation, taking it upon themselves to codify strict data regulations in order to curtail data misuse by banks.

- Regtech spending is expected to reach $76 billion by 2022. The catalyst for this explosion in spending has been the increase in financial regulations, which has prompted banks and other financial institutions to ensure regulatory compliance to avoid massive fines.

- Since the global financial crisis in 2008, banks have been hit with $243 billion in fines. Banks are preemptively attempting to stave off these pernicious fines by investing in regtech, which eliminates the need for massive compliance teams and drives compliance.

- APIs

- Financial data APIs are changing the way the financial services industry looks at banking and have bolstered the concept of open banking as a viable concept. Open banking refers to banks opening up their vast amounts of client data to help financial technology startups develop applications designed to help banking clients.

- Data anonymization is the key to the viability of open banking as a concept, as it means that data is cleansed of any personal information prior to being handed over. This ensures the protection of user privacy and allows companies to use these massive datasets to develop innovative solutions within the financial services space to the benefit of the entire industry. Regulators lead the drive for open banking, creating legislation designed to promote competition and consumer choice by catalyzing innovation in the sector.

- Financial data APIs are multifaceted tools that can be leveraged to provide value in a variety of ways, including connecting businesses to stock information.

- Payments

- Payments is such a massive subcategory within the fintech space it deserves its own article (which it will get, coming soon). The largest subcategory within the fintech space, payments has improved the ease with which people can do business.

- Payments solutions aim to cut down on transaction times between financial institutions, specifically within the international money transfer market, which has been the bane of many entrepreneurs’ existence. Small businesses, by using a payment gateway solutions such as Square, can now accept credit and debit cards, opening up a whole new range of potential customers who deign to use cash.

- Mobile payments in particular has become an increasingly important fintech category that is opening the door to financial inclusion for billions of people.

- Banking

- Banking software has been around for quite some time but has seen rapid development in the past few years, specifically in the mobile banking sector.

- Mobile banking has driven financial inclusion for the 2 billion unbanked or underbanked, enabling these users to skip the step of banking with a brick-and-mortar institution. Mobile banking allows consumers to bank directly on their mobile devices.

- Lending

- Lending technology has also developed rapidly within the fintech framework, offering businesses and consumers opportunities to borrow like never before.

- Lending and loan software improvements have also impacted traditional lending institutions by giving them tools to automate processes, cutting down on the time spent on unnecessarily redundant tasks. From loan origination to loan servicing, solutions in the lending category run the gamut and provide a breadth of functionality specifically for the lending industry.

- A prime example is peer-to-peer lending platforms. While these platforms often offer personal loans, they also offer business loans. The goal of peer-to-peer lending platforms is to lower the qualification barrier to getting loans. Businesses that would otherwise not qualify for a loan from a traditional financial institution have the opportunity to qualify for these.

- Blockchain

- While blockchain is not unique to the financial services industry, it was in the industry in which it was first utilized.

- The premise of blockchain (here is a more in-depth blockchain explained resource) is that all data is housed in a distributed ledger, which ensures the veracity of the data housed there by cross-referencing it against all the other ledgers in existence.

- There are a variety of use cases for blockchain technology within the financial services industry. One estimate puts the potential time savings in just the banking industry at 5.4 million hours per year by 2022.

- While the regulatory powers that be are still working on instituting solid regulations, it looks as though blockchain technology in some form, be it public or private, is here to stay in the financial services industry. Our blockchain platforms category has dozens of products upon which fintech projects can be built.

- Smart contracts

- One blockchain application within the financial services sector is that of smart contracts. A smart contract utilizing blockchain technology validates, monitors, and enforces the terms of the contract automatically. This eliminates the need for legacy technologies in the financial contracts world and streamlines the entire contract process.

The Future of Fintech in Malaysia and Globally

The next few years look to be bright for the fintech industry. Advances in artificial intelligence and data handling and analytics will drive even more innovation in the sector.

Open banking practices and an increase in the number of financial data APIs will drive even more fintech application development. Blockchain projects have the potential to catalyze rapid evolution in the banking industry and beyond.

What are the Career Options for Fintech?

- Entrepreneur

- FinTech Specialist

- Banking Specialist

- Payment System Specialist

- Data Analyst

- Financial Analyst

- Product Developer

- Compliance Expert

- FinTech Quantitative Developer

- Strategy Analyst

- Business Development Associate